Yes! It has come to my attention that there are people among miles and points collectors with credit card debt.

Think I’m kidding? I wish! Let me give you a moment to let it sink in. Because if you’re reading this post and you’re one of those people, well…

You. Must. Stop.

Here are some numbers, according to the U.S. News survey, which are disturbing to me on so many levels.

Almost 50% travel credit card holders have credit card debt

Should we take this survey at face value? No.

If so, is it really that bad? Yes!

True, any survey should be taken with a grain of salt. People don’t necessarily tell the truth even if it’s anonymous. Here is a Gizmodo quote I love about how much you can trust an anonymous survey. Hint: very little.

People lie to surveyors. They always have and they always will. This is why people adjust the number of sexual partners they’ll claim if they’re made to believe that they’re hooked up to a lie detector. It’s why kids will claim they’ve done drugs that don’t exist. There is simply no amount of anonymity that an interviewer can give, no level of assurance that they’ve heard everything before, no guarantee that they just have a dispassionate interest in the facts, which will completely stop people from lying. And that’s when the interviewer is telling the truth about how anonymous the survey is, and how much they don’t personally care what the answer is.

But if everybody lies, why should we care about this survey?

Because when people lie, they tend to come up with the false “right answers.”

Says Gizmodo:

What percentage of your income do you give to charity? If you saw an injured bunny rabbit, would you try to help it? These are questions with a ‘right’ answer.

Not carrying a balance is a perfect example of a “right” answer. If 48.1% of travel credit card holders say they don’t carry a balance, you can bet that some of them are lying. How many? Some researchers suggest “that up to 50 percent of people in any given sample will provide dishonest responses on any given survey.”

Wow, just wow! Even if there is only some truth to that, it’s safe to presume that a majority of travel rewards credit card holders carry a balance on their credit cards at least from time to time.

But don’t we know better than most travel rewards credit card holders?

I’ve always presumed it’s common knowledge. If you can’t or won’t pay your credit card bill in full every month, this game is not for you. Travel is a lifestyle. It’s not OK to finance your lifestyle by going into credit card debt.

“I thought the advice was to never carry a balance!” says a redditor LupineChemist, and continues, as if debunking himself: “(Note that I do from time to time just for cash flow purposes, I know damned well what I’m paying for).”

Hmm, that’s funny. I know at least one other guy who used to feel this way.

Let’s take a short walk down my memory lane

I came to the U.S. in the fall of 1992. The next year, I was lucky enough to enroll in college. Back then, banks would hunt down students to give them a credit card, so I got my first one in 1993. In all honesty, I applied just for laughs (and because they would give me a free t-shirt).

I had no right to get an unsecured credit card – no income, no credit history, no nothing, and yet, I got approved! Imagine my delight. I suddenly possessed this magic card that would open all kinds of doors for me in my new country. Back in Russia, I’d only seen credit cards in pirated American movies, and the power they gave to people was nothing short of magic!

Remember this classic?

“My dad told me specifically I can only use it in case of an emergency.”

“Well, maybe one will come up.”

Never gets old!

Anyway, I quickly got popular, and “rich.” My friends who weren’t so lucky would give me cash for ordering stuff for them (no Internet yet, just the phone orders), and I ran my card like there was no tomorrow. Since I always paid on time, they would regularly increase my credit line without a hitch. Then I would apply for more cards, and my new credit lines would get extended, too.

And in return, I’d only have to pay something like one or 2% of my monthly balance and my benevolent credit card benefactors would even send me these magical “free” checks so I could use my credit card to pay rent, bills, and other expenses – gee, what a bargain…

“You gotta live today!” was a prevailing attitude back then. I heard it everywhere, from my older relatives, friends, their relatives, and their friends. Credit ruled! Everyone I knew would buy cars, TVs, appliances, furniture – everything with plastic and/or “0% financing.” It was so easy that even when I started making some money and was able to pay more, I kept sending them minimum dues every month. Even as my monthly payments grew larger, I still didn’t care. Why would I? I kept getting these free checks and kept borrowing from Peter to pay Paul. Life was great!

And then it came to a screeching halt – fast! And across all my accounts! That will happen inevitably when you keep screwing with your utilization ratio. Suddenly, there were no more blank checks, no more promotional 0% APRs, no “love” from credit cards anymore. I think this is how athletes must feel when they get thrown out for getting “old.”

Suddenly, I was forced to face the mess I’d gotten myself into. There I was, a guy with a college degree, who thought he’d been quite good at math, and I still couldn’t understand for the life of me how these damn numbers added up. When I finally realized I was lost, I called Citibank and I got really lucky. I got a wonderful agent who patiently and expertly explained to me in every small detail what was happening. That one hour on the phone changed my life.

How about a pat on the back?

You tell me! True, I’ve been debt-free for almost 20 years. But not before I lost thousands upon thousands of dollars enriching credit card companies. To add insult to injury, I also lost tens if not hundreds of thousands more in lost opportunities (again, we’re talking about the nineties!). So, somehow, I don’t feel like attaboy. The truth?When I look back I feel like an idiot because you know what — learning from one’s mistakes is overrated. Smart people don’t have to learn from their own mistakes. They learn from mistakes made by others.

What I’m trying to say is this: I don’t see a single scenario where it’s OK to carry a credit card balance, unless you absolutely have to. And there can be unfortunate scenarios when you might absolutely have to, make no mistake about it.

Unless you are honestly making money (not miles or points – money!) using plastic for “cash flow purposes,” you shouldn’t play the miles-and-points game at all! In my Brooklyn office I occasionally run small seminars that set people up for the game. Before I even take their money, I make my potential students promise 3 things:

- They must affirm they can pay their credit card bills in full every month.

- They must promise they will keep it this way.

- They must promise they will stop playing if they can’t.

If you think you can beat the system on the system’s own field, you’re delusional. Unfortunately, a lot of people must use credit cards just to make ends meet (“cash flow purposes,” my ass!). That’s a sad reality, but you gotta do what you gotta do.

I know what you’re thinking. You’re thinking “but I’m flying in First Class, staying at 5-star resorts, and all that for free; how much would that cost me otherwise?” Well, it would cost you exactly zero. Because somehow, you would still be fine without sipping champagne in First or sleeping in an Overwater bungalow.

Grabbing a few free luxuries on the go doesn’t translate into savings. You can’t or at least shouldn’t be paying with your future for unnecessary hedonistic pleasures by getting in credit card debt!

So what to do if you must use credit cards for “cash flow purposes”?

If you must use a credit card to make ends meet, you don’t need this:

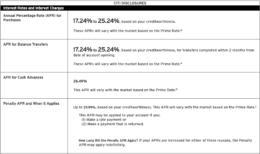

The High APR Citi AA Advantage Card

You need something like this:

The Low APR UFCU Credit Card

Why? Because the Citi AA card will cost you this:

If you carry balance, you will pay at least 17.24% APR.

While the UFCU Best Rate card will cost you this:

Or you can pay 5.90% APR

And before you ask, yes, anyone can join University Federal Credit Union by donating $20 to the Longhorn Foundation.

Just think about it for a moment. How many miles and points would you need to “game” in order to justify over an 11+ percent interest rate difference?

A credit union is not the only way to get a low-APR credit card. Trustmark offers 7.40% APR for excellent credit, although its credit cards are not available in all states. You won’t usually find these offers on credit card aggregators sites, but keep looking and you will find them. Check credit unions first, then some lesser-known banks. Choose cards with no frills – forget frills! Saving hundreds or thousands of dollars a year on interest rates is thrilling enough.

The point is, if you carry a balance on your credit card and pay more than a SINGLE-DIGIT INTEREST RATE you’re lying to yourself. Get out of debt first, review your finances, trim your budget going forward if you must, then come back to the game. But only if you’re prepared to never pay any fees to a credit card again, barring unforeseen circumstances.

And no, an urgent need for a new pimped-up TV or whatever doesn’t qualify.

Photo By: Noemí Galera

Great post, thank you! I appreciate your candid and raw way of presenting this information. I hope your post gets picked up by a few blogs to get more readers, as everyone can benefit from reading it.

Cheers,

PedroNY

Pedro, thanks for your kind words. I felt it needed to be said as we are back in debt the way we were right before 2008. And seeing how some folks who should know better are doing the same thing… Unnerving.

Great article!! WSJ posted an article recently on credit card debt and it’s mind-blowing how much credit card debt the average American has. I love your recommendation on getting a low APR such as UFCU. Do you have any data points on what the credit limit may be? I have 745-760 credit limit, depending on the bureau, and thinking about getting the UFCU card. I want a credit limit like the the bigger banks gives (20k+) so if I carry a balance, my credit utilization will stay under 30%. Thanks!

Thanks! Unfortunately, I don’t know much about UFCU, I just like the low APR and the fact that it’s easy to join. You have a very good to excellent credit, so I don’t think you would have a problem getting a card. As for a credit limit, that heavily depends on your income and other variables, but in general, credit unions tend to be more conservative than big banks.

Not to overlook the regular opportunities to carry a balance at zero percent interest for an introductory period–sometimes for as long as a year or more.

Of course you have to have cash to repay when the intro period ends, and the interest rate skyrockets.

These are useful for actual cash flow (meaning cash will be available but isn’t now) and also valuable if you have an investment use for the borrowed funds.

Good point! And you might even be able to negotiate a few months of 0% APR on an existing account. Gotta be very careful, though.

That’s something I always wonder… how many people get into this game and end up getting into bad debt? Having the possibility of using all that credit you have available is very risky. It’s hard to get the numbers so your writing about the surveys is very interesting too.

Yes, something to think about, definitely. This is not a harmless hobby, and the odds of making costly mistakes are fairly high. Thanks for your comment!